In 2023, the global fashion industry will need to weather inflation while finding opportunities in shifting consumer patterns, channel and digital marketing strategies, and manufacturing approaches.

After 18 months of strong growth (early 2021 to mid-2022), the fashion industry is once again facing challenges. Hyperinflation and sluggish customer sentiment have already led to a decline in growth rates in the second half of 2022. Those involved expect that this slowdown could continue into 2023.

However, many industry players are in a stronger position than they were a year ago. The fashion industry achieved 21% revenue growth in 2020-21, with EBITA margins doubling by 6 percentage points to 12.3%.

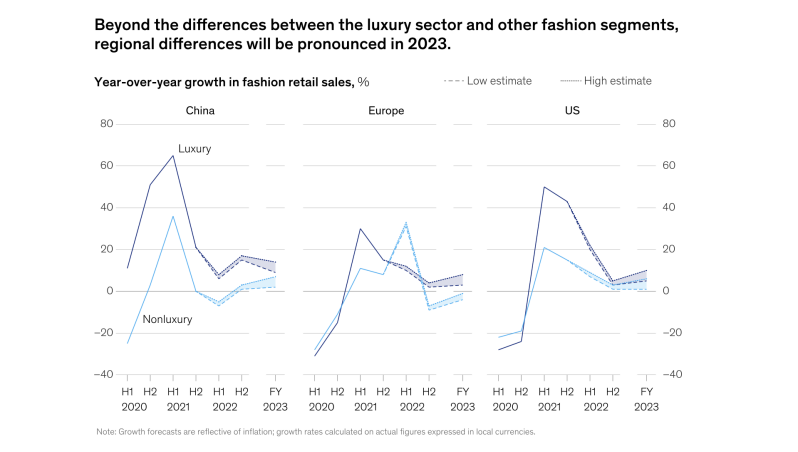

Looking ahead, the sector expects the luxury goods industry to outperform other sectors as affluent shoppers continue to travel and spend, thus becoming more insulated from severe inflation. According to McKinsey's analysis of fashion forecasts, the luxury sector is expected to grow by 5% to 10% in 2023, driven by strong momentum in China (expected to grow by 9% to 14%) and the US (expected to grow by 5% to 10%). On the other hand, Europe is under high pressure from currency exchange rates and a growing energy crisis, which could lead to moderate sales growth in the luxury sector (expected to grow between 3% and 8%).

Excluding the luxury sector, the fashion market will struggle to achieve significant growth in 2023. McKinsey's analysis of fashion forecasts predicts relatively slow sales growth of between -2% and +3%, driven by a contraction in Europe (expected to shrink by 1% to 4%) . China and the US are expected to fare better, with growth of 2% to 7% and 1% to 6% respectively. These forecasts reflect inflation and are in local currency, meaning that the actual impact on the industry may be more negative than these figures suggest.

These are just some of the findings from The State of Fashion 2023, a joint report by Business of Fashion and McKinsey. The seventh in an annual series, the report discusses the key themes shaping the fashion economy and assesses a range of possible responses. It reflects in-depth research and multiple conversations with industry leaders to reveal the key trends likely to shape the fashion landscape in the year ahead.

Fig.1 The State of Fashion 2023: Holding onto growth as global clouds gather(2022)

Ten themes for 2023

This year’s report presents a difficult outlook ahead, as fashion companies face challenges and revise forecasts downward after an exceptionally strong 2021, per McKinsey analysis of global data in the fashion industry. Inflation and geopolitical concerns dominate the agenda for 2023, negatively affecting both consumer demand and brands’ operating costs. Consumers are adjusting their behaviors, as many trade down to cheaper or discounted items to reduce their spending, though the luxury sector will remain strong, with affluent consumers less heavily affected by inflation.

The challenges of the global fashion industry today and in the future

Fashion companies that can adapt to the increasing complexity by updating their operating models and adjusting their strategies for supply chain, sales channels, and digital marketing will be best placed to weather the upcoming storm. They can lean into the following ten emerging consumer trends:

- Global economy:

- Global fragility. Amid the highest inflation in a generation, rising geopolitical tensions, climate crises, and sinking consumer confidence in anticipation of an economic downturn, the global economy is in a volatile state. Fashion brands will need careful planning to navigate the many uncertainties and recessionary risks that lie ahead in 2023.

- Regional realities. Understanding where to invest around the world has never been easy, but rising geopolitical uncertainty and uneven economic recoveries related to the COVID-19 pandemic, among other factors, will likely make it even more challenging in 2023. Brands can reevaluate regional growth priorities and hone their strategies so that they are more tailored to the geographies in which they operate.

- Consumer shifts:

- Two-track spending. Consumers may be affected differently by the potential economic turbulence in 2023. Depending on factors such as disposable income level, some will postpone or curtail discretionary purchases; others will seek out bargains, increasing the demand for resale, rental, and off-price products. Fashion executives should adapt their business models to protect customer loyalty and avoid diluting their brands.

- Fluid fashion. Gender-fluid fashion is gaining greater traction amid changing consumer attitudes toward gender identity and expression. For many brands and retailers, the blurring of the lines between men’s wear and women’s wear will require rethinking their product design, marketing, and in-store and digital shopping experiences.

- Formal wear reinvented. Formal attire is taking on new definitions as shoppers rethink how they dress for work, weddings, and other occasions. While offices and events will likely become more casual, special occasions may be dominated by statement-making outfits that consumers rent or buy to stand out when they do decide to dress up.

- Fashion system:

- Direct-to-consumer reckoning. Although brands across price segments and categories have embraced digital direct-to-consumer channels, mounting digital marketing costs and e-commerce readjustments have put the viability of the model into question. To grow, brands will likely need to diversify their channel mix, including wholesale and third-party marketplaces, alongside direct-to-consumer models.

- Tackling greenwashing. As the industry continues to grapple with its damaging environmental and social impact, consumers, regulators, and other stakeholders may increasingly scrutinize how brands communicate about their sustainability credentials. If brands are to avoid greenwashing, they must show that they are making meaningful and credible change while abiding by emerging regulatory requirements.

- Future-proofing manufacturing. Continued disruptions in supply chains are a catalyst for a reconfiguration of global production. Textile manufacturers can create new supply chain models based around vertical integration, nearshoring, and small-batch production, enabled by enhanced digitization.

- Digital marketing reloaded. Recent data rules are spurring a new chapter for digital marketing as customer targeting becomes less effective and more costly. Brands will need to embrace creative campaigns and new channels, such as retail media networks and the metaverse, to achieve greater ROI on marketing spend and to gather valuable first-party data that can be leveraged to deepen customer relationships.

- Organization overhaul. Successful execution of strategies in 2023 will in part hinge on a company’s alignment around key functions. Fashion executives need a new vision for what the organization of the future will require, focusing on attracting and retaining top talent, as well as on elevating teams and critical C-suite roles to execute on priorities such as sustainability and digital acceleration.

Fig.2.Illustration by Marie Victoire de Bascher for BoF.

Opportunities for the global fashion industry today and in the future

Bereft by global risks and uncertainties, leaders in the fashion industry will need to pay careful attention to macroeconomic and political issues in the regions where they produce and sell their products in the year ahead. They will need to develop risk mitigation strategies that can be implemented quickly as conflicts, fiscal policies, and government regulations evolve. Additionally, they will need to think critically about where they operate, looking beyond top-line growth potential when evaluating new and existing foreign markets. Brands can no longer plan on complete political neutrality as their global customer bases become more connected and outspoken.

In 2023, consumers will be unpredictable and fickle. Brands will need to consider carefully the factors that affect shopping behaviors and respond accordingly. Even as many customers reduce spending, brands have an opportunity to keep customers engaged through, for example, rental channels and off-price retailers. But these strategies will require careful execution to ensure that margins and brand reputations are protected. At the same time, brands will need to update their merchandising and design approaches to reflect shifting ideas around gender lines in fashion and dress codes. Daily office attire will become more casual, and special-occasion dress will become bolder.

Despite the economic headwinds ahead, fashion leaders are in a unique position to reevaluate the ways that their brands produce, distribute, and market their collections. Supply chains remain disrupted from the COVID-19 pandemic, elevating the need to invest in faster and geographically closer manufacturing systems. While direct-to-consumer, digital channels remain a top priority, fashion industry leaders will need to diversify their sales channels to maintain efficiency and market relevance. And finally, brands will need to be more creative in marketing to attract customers through bold, differentiated content that cuts through a crowded digital environment in which data targeting is no longer effective. To execute these changes and respond better to forthcoming regulations around sustainability marketing, the fashion industry should rethink how it allocates talent, promotes, and establishes executive roles and teams—reflecting the key challenges facing the industry in the years ahead.

The outlook for the global fashion industry in 2023 is uncertain and tenuous. Many customers are reigning in their budgets after months of discretionary spending. Growth has slowed in China, and major questions loom about the market’s future trajectory. An energy crisis is disrupting European economies. While the luxury and sportswear sectors have dominated the industry’s list of super successes in recent years, macroeconomic context might change that in the upcoming year. Heading into 2023, the industry’s decision makers will need to prepare to make strategic sacrifices while investing in agility and creativity to succeed when the market eventually recovers.

summary

The global fashion industry forecast for 2023 shows that the apparel industry is not a very promising state for recent graduates, especially for international students, who lack language skills The innate lack of being a native causes the inability to sometimes express what they really want to say in depth very well. And if their own skills do not compare particularly favourably with those of their peers, they lose the competitive edge in the marketplace. This is why fresh graduates with a lot of ambition are not able to make it big in their field of expertise.

It is not only luck but also their own abilities that enable fresh graduates to face opportunities in the job market. Based on data analysis and fieldwork, I found that the garment industry in China is developing regionally, mainly because China is still a developing country and in a state of learning. Therefore, if I were to consider employment, many people would prefer to stay in the UK or go to France for the development of the industry. So if China wants to dominate the apparel market then it should continue to strengthen its brand innovation and it is more important to increase the advantages of self-employment, which was mentioned in Diana Pasek-Atkinson's and NTU ENTERPRISE's lectures on the advantages and disadvantages of freelancing.

Inspired by Diana Pasek-Atkinson'sNTU ENTERPRISE's lectures

List Of Illustrations

Fig.1.The State of Fashion 2023: Holding onto growth as global clouds gather(2022) [Online].Available at; https://www.mckinsey.com/industries/retail/our-insights/state-of-fashion

Fig.2.Illustration by Marie Victoire de Bascher for BoF.[Online].Available at; https://www.businessoffashion.com/reports/news-analysis/the-state-of-fashion-2023-industry-report-bof-mckinsey/

Add comment

Comments